You can't visit the site from Dubai or London. But you can read the balance sheet from anywhere. Why developer-grade analysis is the foundation of every SuperLuxeRE recommendation — across every Indian city.

Written by

Himanshu Bamola

Founder & Principal Analyst, SuperLuxeRE · 16+ years in ultra-luxury real estate strategy

Himanshu advises HNIs, NRIs, and family offices on India's most complex luxury real estate decisions — from Golf Course Road to Worli. His market analysis is trusted by buyers across Singapore, Dubai, London, and the US.

The Big Picture

The Brand on the Brochure Is Not the Risk. The Balance Sheet Behind It Is.

Every year, a meaningful share of NRI and HNI capital that enters Indian real estate is allocated on the strength of three things: a location that sounds familiar, a render that looks impressive, and a price that seems competitive against what the same money buys in Singapore, Dubai, or London. None of these three things — location familiarity, visual presentation, or relative pricing — has any bearing on whether the project gets delivered on time, to the promised specification, by the developer named on the brochure.

For an investor sitting in Singapore, Dubai, London, or San Francisco, this asymmetry is structural and unavoidable. You cannot drive past the construction site every weekend to check progress. You cannot sit in on the developer's board meetings. You cannot read the regional newspaper for early warning signs of a project in trouble. What you can do — what every serious NRI, HNI, and family office investor in Indian real estate should do — is anchor every decision to a single question that correlates more strongly with successful outcomes than any other factor: is this a Grade A developer, and is this specific project structured the way Grade A developers structure their projects?

SuperLuxeRE Analysis

- Across every market we cover — Gurugram, Mumbai, Delhi, Noida, Bangalore, Dubai — the single strongest predictor of on-time, on-spec delivery is not the city, the corridor, or even the specific project. It is the developer's institutional grade: listed status, balance sheet depth, independent construction partnerships, and multi-city delivery history.

- NRI and HNI investors face a structural information gap that domestic buyers do not — no ability to physically monitor construction, attend RWA meetings, or pick up market chatter about a developer's financial health. This makes developer-grade due diligence not a preference but a necessity.

- Family offices in particular evaluate Indian real estate against a global opportunity set — and the comparison that matters is not "is this cheaper than London," it is "does this asset class, in this specific structure, meet the same governance and reporting standards as our other holdings." Grade A developers are the only ones that come close.

- Every project SuperLuxeRE features across India — regardless of city or corridor — passes through the same developer-grade filter before any pricing, lifestyle, or appreciation analysis is even produced. This is the foundation layer, not an afterthought.

Why Developer Grade Matters More for Offshore Investors Than for Anyone Else

A resident Indian buyer evaluating a project has access to information channels that an offshore investor simply does not. They can visit the site unannounced. They can talk to existing residents of the developer's other projects. They can read local news coverage of the developer's financial standing. They can sense, through dozens of small social signals, whether a project "feels" like it is on track.

None of this is available to an NRI in Dubai, an HNI in Singapore, or a family office in London evaluating a ₹15–50 crore allocation to Indian real estate. The information asymmetry is total. And in the absence of ground-level information, the only reliable proxy is institutional structure — because institutional structure is observable from anywhere in the world, through public filings, stock exchange disclosures, and verifiable delivery history.

| Information Source | Available to Resident Buyer | Available to NRI / HNI / Family Office |

|---|---|---|

| Physical site visits | ✓ Routine | ✗ Rare or impossible |

| Local market chatter / RWA networks | ✓ Accessible | ✗ Not accessible |

| BSE/NSE quarterly disclosures | ✓ Available | ✓ Available globally — equal access |

| RERA filings (land cost, project cost, timelines) | ✓ Available | ✓ Available globally — equal access |

| Multi-city delivery track record | ✓ Available | ✓ Available globally — equal access |

The pattern in this table is the entire argument: the information sources that remain equally accessible to an offshore investor are exactly the sources that constitute "developer grade." A resident buyer's local advantage evaporates the moment the question shifts from "does this feel right" to "what does the balance sheet and delivery record show" — and on that question, an investor in Dubai with access to public filings is on equal footing with a buyer in Gurugram. This is precisely why developer-grade analysis is the most powerful tool available to offshore investors specifically.

What "Grade A" Actually Means — A Pan-India Framework

"Grade A developer" is not a marketing term. It is a specific, checkable set of structural characteristics that apply identically whether the project is in Gurugram, Mumbai, Bangalore, or Pune.

| Criterion | What It Means | Why It Matters Pan-India |

|---|---|---|

| Listed on BSE / NSE, or FDI-backed with parent disclosures | Quarterly financial and construction disclosures are mandatory and public | Identical reporting standard whether the project is in Gurugram, Mumbai, or Bangalore |

| Independent construction partner | A separate, large-scale contractor (e.g., Tata Projects, L&T) with its own balance sheet executes construction | Removes single-point dependency on the developer's cash position for construction continuity |

| Multi-city, multi-decade delivery record | The developer has delivered projects across multiple cycles, in multiple cities, without major stalled projects | A track record built across geographies and downturns is structurally more reliable than one built in a single boom-cycle market |

| RERA land cost proportionate to total project cost | Land cost as filed in RERA represents a sound proportion (typically 30–40%) of total declared project cost | Signals the project was underwritten on sound economics rather than land speculation funded by buyer pre-sales |

| Back-loaded or milestone-linked payment plans | A meaningful share of payment falls at later construction stages, not concentrated at booking | Reduces buyer's exposure if early-stage delays occur, and reduces developer's dependency on buyer cash for early construction |

Notice that none of these five criteria mention a city, a corridor, or a price point. That is the point. A Grade A developer applying these structures in Mumbai is applying the same structures in Gurugram, Bangalore, or Pune. This is what makes developer-grade analysis genuinely portable across SuperLuxeRE's pan-India coverage — the framework does not need to be rebuilt for each city.

Why Family Offices Specifically Need This Filter

Family offices allocate to real estate as part of a broader portfolio that includes listed equities, private equity, fixed income, and increasingly, global real assets. The governance standard applied to every other asset class in that portfolio — audited financials, board oversight, regulatory disclosure — has historically had no equivalent in Indian real estate, where a significant share of developers have been private, family-run businesses with limited external reporting.

Grade A developers close this gap. A family office allocating to a BSE-listed developer's project is, for the first time, applying the same due diligence framework to Indian real estate that it applies to every other holding — public financials, disclosed liabilities, independent audit, and a delivery record that can be verified without a site visit. This is not a minor convenience. For many family offices, it is the difference between Indian real estate being an investable asset class and being an inaccessible one.

- Governance parity: Listed developer disclosures can be reviewed by the family office's existing research team using the same frameworks applied to other equity holdings

- Liquidity context: Grade A developer projects, even though the underlying asset (property) is illiquid, sit within a more liquid secondary market — because brand recognition drives resale demand

- Reputational alignment: Family offices increasingly consider the reputational profile of co-investors and developers — Grade A names carry lower headline risk

- Cross-border comparability: A family office with holdings in London, Singapore, and Dubai can evaluate a Grade A Indian developer's project against the same disclosure standards as a developer in those markets — Grade B and below developers typically cannot be evaluated this way

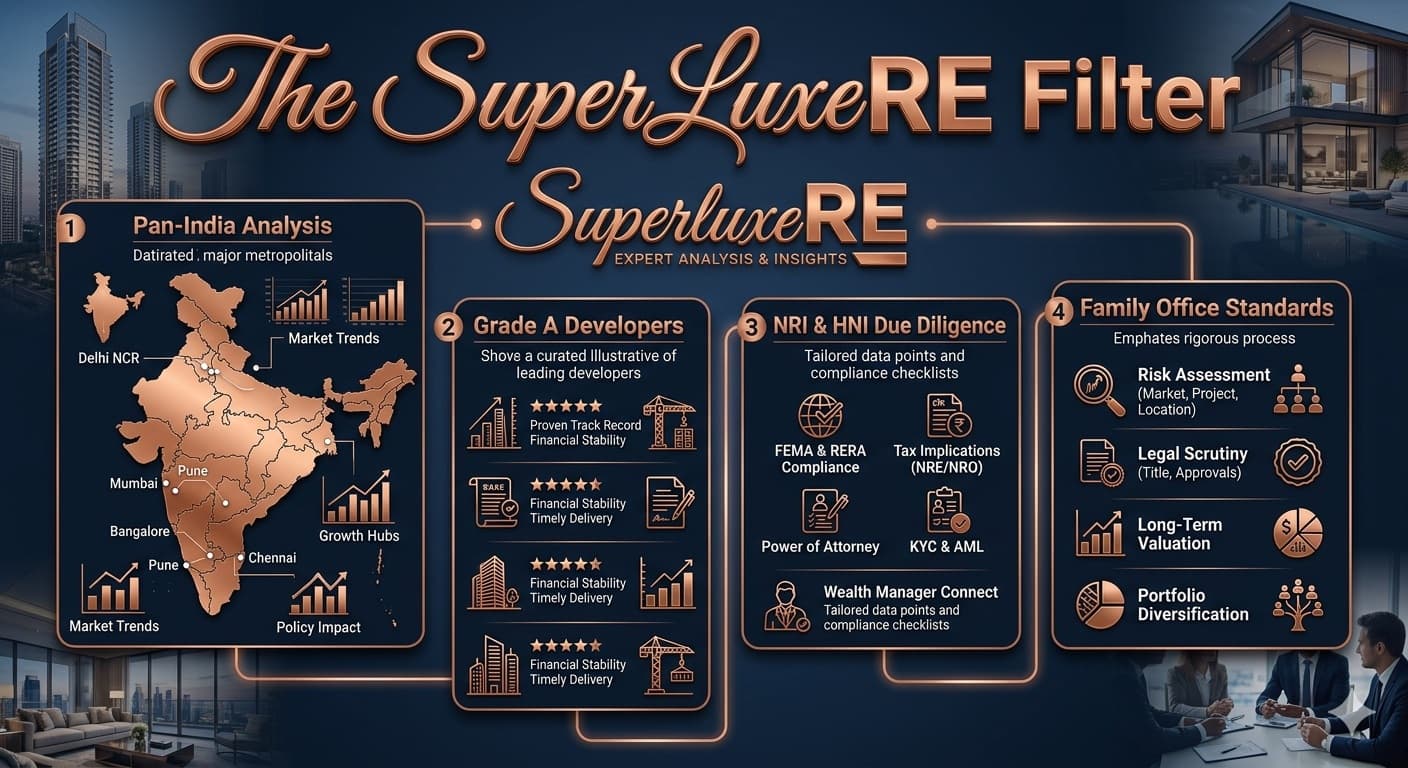

The SuperLuxeRE Process: How Every Recommendation Is Built

This is why every project SuperLuxeRE features — regardless of city — goes through the same sequence before it reaches a recommendation to an NRI, HNI, or family office client:

| Step | What We Check | Outcome |

|---|---|---|

| 1. Developer Grade | Listed status / FDI backing, multi-city delivery history, financial disclosures | Projects from developers below this threshold are not featured, regardless of location or price |

| 2. Project Structure | Construction partner, RERA land cost ratio, payment plan structure | Identifies whether this specific project follows the developer's institutional norms or is an outlier |

| 3. Location & Corridor Analysis | Connectivity, social infrastructure, corridor appreciation history, supply pipeline | Determines the location-specific investment thesis — only evaluated after developer grade clears |

| 4. All-In Cost & Yield Modelling | Base price, PLC, GST, stamp duty, registration, fit-out (if bare shell), rental comparables | Produces the true cost and return profile — not the headline PSF |

| 5. NRI / Family Office Specific Factors | FEMA compliance, repatriation rules, LTCG implications, POA process for remote transactions | Confirms the transaction can be executed remotely with full regulatory clarity |

This sequence is identical whether the project under review is on Golf Course Road in Gurugram, on the Noida Expressway, in South Mumbai, or on Bangalore's outer ring road. The city changes. The filter does not. This is what allows SuperLuxeRE to make pan-India recommendations with the same confidence level in each market — the underlying due diligence framework is geography-agnostic by design.

The SuperLuxeRE Filter

The Developers Whose Projects Clear Our Bar — Across Every City We Cover

This is not an exhaustive list, and it is not static — but these are the names that consistently meet the structural criteria above across multiple cities and cycles. When we feature a project from one of these developers, the developer-grade question is already answered. The analysis that follows is about the project, the location, and the numbers — not about whether the foundation is sound.

Each operates across multiple Indian cities, carries listed or institutionally-backed financial transparency, and has a delivery record that spans more than one market cycle. For an offshore investor, a project from any of these names starts from a position of structural confidence that a Grade B or unlisted developer's project — however attractive the renders — simply cannot offer on day one.

See the Filter Applied

For an NRI in Dubai, an HNI in Singapore, or a family office in London, the question "is this a good investment" cannot be separated from the question "can I actually verify any of this from where I am sitting." Location, lifestyle, and pricing analysis matter — but they are built on top of a foundation, and that foundation is the developer's institutional grade. A beautiful project from a Grade B developer is a beautiful risk. A modest project from a Grade A developer is a modest, verifiable commitment.

This is why SuperLuxeRE applies the same developer-grade filter to every market we cover — Gurugram, Mumbai, Noida, Bangalore, and beyond. It is the one part of our analysis that does not change with the city, because the principle does not change with the city. For offshore capital with limited ability to verify on the ground, this filter is not a nice-to-have. It is the entire basis on which a remote, multi-crore commitment can be made with confidence.

Frequently Asked Questions

Q1. What does "Grade A developer" mean in Indian real estate?

A Grade A developer is one that meets a specific set of structural criteria: listing on BSE/NSE (or equivalent FDI-backed institutional structure with public disclosures), use of independent large-scale construction partners with their own balance sheets, a multi-city and multi-cycle delivery record without major stalled projects, RERA-disclosed land costs proportionate to total project cost, and payment plans that are back-loaded or milestone-linked rather than front-loaded. This is a structural classification, not a marketing term — and it can be verified through public filings from anywhere in the world.

Q2. Why is developer due diligence more important for NRI and family office investors than for resident buyers?

Resident buyers have access to information channels — site visits, local market chatter, RWA networks, regional news — that offshore investors structurally cannot access. For an NRI in Dubai or a family office in London, the only information sources that remain equally accessible are public filings: BSE/NSE disclosures, RERA filings, and verifiable multi-city delivery records. These are exactly the sources that determine a developer's "grade" — making developer-grade analysis the most powerful and most accessible due diligence tool for offshore investors specifically.

Q3. Which developers does SuperLuxeRE consider Grade A?

SuperLuxeRE applies this filter to developers including DLF, Godrej Properties, Oberoi Realty, Experion, Max Estates, and Mahindra Lifespaces — each of which operates across multiple Indian cities, carries listed or institutionally-backed financial transparency, and has a delivery record spanning more than one market cycle. This list is illustrative of the standard, not exhaustive — the underlying criteria, not the specific names, are what define the filter.

Q4. How does this developer-grade filter apply across different cities — does it change for Mumbai vs Gurugram vs Bangalore?

No — the five structural criteria (listed status, independent construction partner, multi-city delivery record, proportionate RERA land cost, back-loaded payment plans) apply identically regardless of city. This is what makes the framework genuinely pan-India: a Grade A developer's project in Mumbai is held to the same structural standard as their project in Gurugram or Bangalore. Location-specific analysis — connectivity, social infrastructure, corridor appreciation — happens only after the developer-grade question is answered.

Q5. Why do family offices specifically need this kind of analysis for Indian real estate?

Family offices apply governance standards — audited financials, disclosed liabilities, independent oversight — to every asset class in their portfolio. Historically, much of Indian real estate (private, family-run developers with limited reporting) had no equivalent. Grade A developers close this gap: their public disclosures can be reviewed using the same research frameworks a family office applies to its equity holdings, making Indian real estate genuinely comparable to other asset classes in the portfolio for the first time.

Q6. Does choosing a Grade A developer guarantee a project will be delivered on time?

No — no developer grade eliminates all risk, and macro conditions (such as construction cost inflation or supply chain disruption) can affect even well-capitalised projects. What Grade A status provides is structural resilience: the balance sheet depth, independent construction accountability, and transparency to absorb shocks and communicate delays publicly, rather than the project simply stalling without disclosure. It significantly improves the probability of on-time, on-spec delivery — it does not make it a certainty.

Pan-India Advisory, Built on One Consistent Standard

Whether your allocation is in Gurugram, Mumbai, Noida, or Bangalore, SuperLuxeRE applies the same developer-grade due diligence before any recommendation reaches you. Speak with us about your portfolio's real estate allocation.

📞 +91-9873336686 | 📧 aspire@superluxere.com | 🌐 superluxere.com

Sources: SuperLuxeRE Analysis.

Published by SuperLuxeRE

India's Luxury Real Estate Intelligence Partner

📞 +91-9873336686 | 📧 aspire@superluxere.com | 🌐 superluxere.com

Tagged: